Property has produced extraordinary investment returns for New Zealanders over the last decade. Many investors see the high returns that have been fuelled by declining interest rates.

Until recently, the average house price increased by more than 30%, fuelled by the fact that in the last two years declining interest rates have meant that affordability has remained unchanged. With increasing inflation, we will have increased interest rates which will have the single largest impact on people’s ability to afford property. This will be compounded with our Government’s many different restraints to rein in property investment.

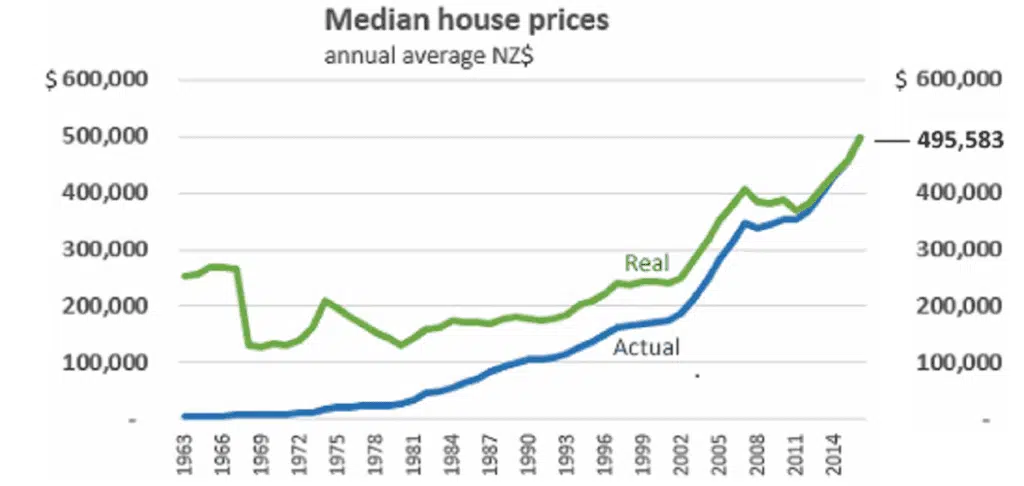

Historic property trends (growth)

Booster (a default KiwiSaver provider) states that the average increase in property values between 1971 and 2019 was 8.8% year on year. This is in line with anecdotal evidence. A house in 1971 may have sold for $10,000, and in 2019 that comparable house may have sold for $580,000. However, an average house in 1971 would be significantly less desirable than an average house in 2019. Simple things like heat pumps, insulation, and fixtures have changed. Whilst house prices have increased so too has our standard of living. This approximation of growth takes ‘nominal’[1] value to the extreme.

House price growth is only a relatively recent phenomenon for New Zealand. Interest.co.nz compares the ‘nominal’ home value to the ‘real’[2] home value. From 1963 to 1981 the ‘real’ value of property was decreasing whilst the ‘nominal’ value was increasing. From 1963-2002 there was virtually no change in the ‘real’ value of property.[3]

Of course, you also need to account for expenses such as rates, insurance, upkeep. Typically, we don’t include mortgage expenses or costs of renovations in these calculations and other expenses related to tenancy. 2% is a reasonable estimate that will be spent on property each year to own it. This will vary on location and the age of the property (you normally pay a premium for a newer property but it will have less maintenance in the first decade).

When we consider the long-term nominal return from property, we (Lyfords) normally forecast growth of 4% which may leave 2-3% on the table as a margin of error. Indeed, this is what we experienced from Feb 2017 to 1 August 2019, during which we had property growth of 3.1% which was a more typical growth period.[4]

What drives property growth?

There are three primary factors that drive property growth;

- The need for supply

- Changing interest rates

- Changing legislation

The need for supply

In recent years housing supply has not met demand.

Changing legislation has resulted in new homes costing more to build. These changes led to a lack of property development creating a deficit in the market resulting in rising demand. Now that house prices have caught up to building costs it is profitable again to build new property. House consents have quadrupled over the last decade. Economists forecast that the housing deficit will be eliminated by the end of this year.

Note the dip in 2007, in the graph above. The requirements for double glazing were introduced at the same time. There has been a steady increase in building consents since 2011. If this trend continues it follows that there will eventually be an oversupply of new homes. This is more certain as changing legislation has made it easier for new builds.

We see that the demand for new property in New Zealand will continue to reduce over the foreseeable future.

Stuff.co.nz has recently summarised[5] how well we are placed to achieve these figures. Stuff.co.nz estimated that we needed 107,000 new houses within the next 30 years. They showed all the areas where new homes would be built and published the number of houses built in Wellington over the last 6 years. Last year Wellington regional councils consented 4,019 new dwellings which is enough to meet the demand of 120,000 houses (over the next 30 years). Interestingly, the number of new consents has increased by 10% per year for the last 6 years. With recent changes to zoning this may increase. There is strong evidence to show that we no longer have any demand issues left in our housing.

Changing Interest Rates

The Covid Pandemic reset global supply chains. Prior to the Pandemic, New Zealand like many countries, was dealing with our increasingly inter-connected economy which reduced inflation figures. In order to combat the reduction in inflation, the RBNZ (Reserve Bank of New Zealand) had lowered interest rates consistently since the 2008 economic crisis.

When the Pandemic resulted in New Zealand’s first lock down the RBNZ further reduced interest rates in order to encourage consumer spending. Almost everyone was predicting a decline in the property market but as finance was so cheap, property became more affordable so many people became able to purchase higher value homes ultimately resulting in soaring demand and further compounded by the FOMO (Fear Of Missing Out) effect.

The New Zealand Government assisted consumers to spend more by financing businesses adding billions of dollars to the economy. The cost of doing so was more than $70,000,000,000.

Businesses have had to deal with logistical challenges which have further increased prices and increased the profits for businesses. The results of the Government stimulus have resulted in an inflation rate of 7.6% pa; the highest it has been in 30 years. With high inflation, rising interest rates follow.

It’s staggering to see the results in the graph below on mortgage affordability. This graph shows that even though house prices have increased, affordability remains similar. Deposits, however, have significantly increased so there is a larger entry requirement for first home buyers. Once you have a mortgage the affordability is very similar to 2010 when house prices were half as much as they are now. The difference here is that interest rates were above 7%.[6]

New Zealand’s property market is now worth $1.72 trillion which is ($1,720,000,000,000).

The ANZ Bank predicts interest rates to rise to 7.4%[8] fuelled by many factors including the war in Ukraine. Most economists expect this relatively high rate to be short-lived but inflation of 5% p.a. may be persistent for many years. It’s likely that higher than average inflation will be persistent for the next 4 years; inflation has momentum which is hard to undo. The RBNZ makes small adjustments to the OCR (Official Cash Rate) in an attempt to control inflation.

When interest rates increase to 5%-7% this will heavily impact the affordability of property. It’s unknown how long interest rates will remain high but the effect will linger.

Increasing interest rates will reduce property affordability which is likely to be the single largest factor to impact property values in New Zealand. In addition, if the ‘nominal’ value of property reduces there will be an immediate effect on buyer confidence which could quickly change consumer spending attitudes and create a negative inflationary environment. The possibility of negative inflation is unlikely to be the dominant factor reducing our inflation as it’s mostly generated by our import market currently. The RBNZ prefers to have positive rather than negative inflation.

Changing legislation

Legislative changes have direct consequences for investors and the general property owner. Changing legislation includes the new in-fill rules, KiwiSaver, the CCCFA (Credit and Consumer Contracts Finance Act), RBNZ (Reserve Bank of New Zealand) lending rules, local body rules, the interest deductibility changes, etc.

The CCCFA has already had enormous effects on those looking to apply for mortgages, even well-off individuals are noting that the hurdles to applying for a loan are more significant. The CCCFA was a very unpopular piece of legislation. It has since been reviewed to make it less restrictive, however, the effects of the CCCFA have had already had an impact. In the short term it seemed to be the brick wall that the property market needed.

Interest deductibility has been a small dampener for property investors, significantly changing their yields, however, it didn’t have the full effect that the Government expected. National supply of rentals is down by 12%[9] and rents have increased accordingly. Rental yields now have significant room for growth, albeit reduced by the interest deductibility.

First Home Buyer Grants via KiwiSaver have reduced due to the price limitations to purchase first homes. It’s expected that this will be re-examined so that first home buyers have more assistance to purchase.

In-fill housing will be one of the biggest detractors to property valuations in the coming years. In-fill housing will enable more houses to be built on most properties in New Zealand with very few restrictions from the local Council. There will be more spaces to build property and we expect consents to continue to increase. Properties with large sections may experience an increase in value but most will simply be affected by the reduced demand for property.

We don’t expect legislation to have further negative effects on the property market in the foreseeable future as the Government has probably realised their ‘success’. The on-going effects will persist until an equilibrium has been reached and this will likely balance the effects of new legislation assisting first home buyers.

Property forecasts

Property values are expected to reduce by 25-30% in ‘real’ dollars over the next 4 years.

By the end of 2022 the New Zealand property market is expected to shrink by 10%, by ‘nominal’ figures, and remain relatively flat for a further 3 years before returning to the historical average of 4% ‘nominal’ growth. A nominal figure includes inflation.

A flat property market compounded with higher than normal inflation will devalue real property values.

Real estate agents now agree that the decline is in full effect[10]

The decline in ‘real’ property values may not necessarily translate to increased affordability. The rate of future property growth will relate to long-term inflation rates which at this stage are too difficult to predict. From a global economic perspective, we can expect that infrastructure will recover to where demand needs it to be potentially resulting in a steep drop in inflation. Which may lead to decreasing interest rates in 4 years and a improving affordability index.

Beyond 2026 there will be strong property construction and more attainable finance. The two opposed factors create a lot of uncertainty in the long-term property outlook. With increased supply and easier finance first home buyers are likely to benefit significantly.

The New Zealand property market is extremely resilient. Typically, investors and owner occupiers would rather hold onto a property over taking a loss in the market. This makes the expectation of a short-term dip above 10% very unlikely. House prices need to come down, relative to where they sit as an investment, and in order to do that with investors refusing to make losses, higher inflation will be required.

[1] Nominal means the face value of an asset and is not adjusted for inflation.

[2] Real means the value of an asset adjusted for inflation.

[3] interest.co.nz article on house prices past four years

[4] Real Estate Institute NZ

[5] Stuff.co.nz article on Wellington house prices

[6] Infometrics on housing affordability

[7] Figures are from the Reserve Bank of New Zealand and are to Jan 2021 only

[8] Newshub on inflation predictions

[9] Stuff.co.nz article on rental prices

[10] Newshub .co.nz article on real estate agents and house prices